8

How Crypto Exchanges Implement AML: A Technical and Regulatory Guide

Imagine running a digital gold mine where anyone in the world can trade, but you have no idea if your customers are legitimate investors or international criminals. For years, many digital asset platforms operated in a grey area, but the party ended around 2019. That was when the SEC, the U.S. Securities and Exchange Commission, and other regulators stepped in to make it clear: if you run a crypto exchange, you are a financial institution. This means you can't just ignore where the money comes from. You need a robust Crypto AML implementation strategy or risk facing massive fines and jail time.

The Blueprint for Compliance: The FATF Framework

Most exchanges don't just guess how to stop money laundering; they follow the playbook written by the FATF, or the Financial Action Task Force. This international body sets the global standards that keep the financial system from becoming a playground for terror financing. To stay legal, exchanges generally split their efforts into three main buckets: identifying the user, watching the money, and reporting the red flags.

First, there is the identity phase. This is where the exchange confirms that you are who you say you are. Second, they move into ongoing monitoring. Since crypto moves 24/7, the surveillance can't sleep. Finally, they have a response protocol. If a user suddenly deposits ten million dollars in Monero and tries to move it to a high-risk jurisdiction, the exchange must have a process to freeze those funds and alert the authorities.

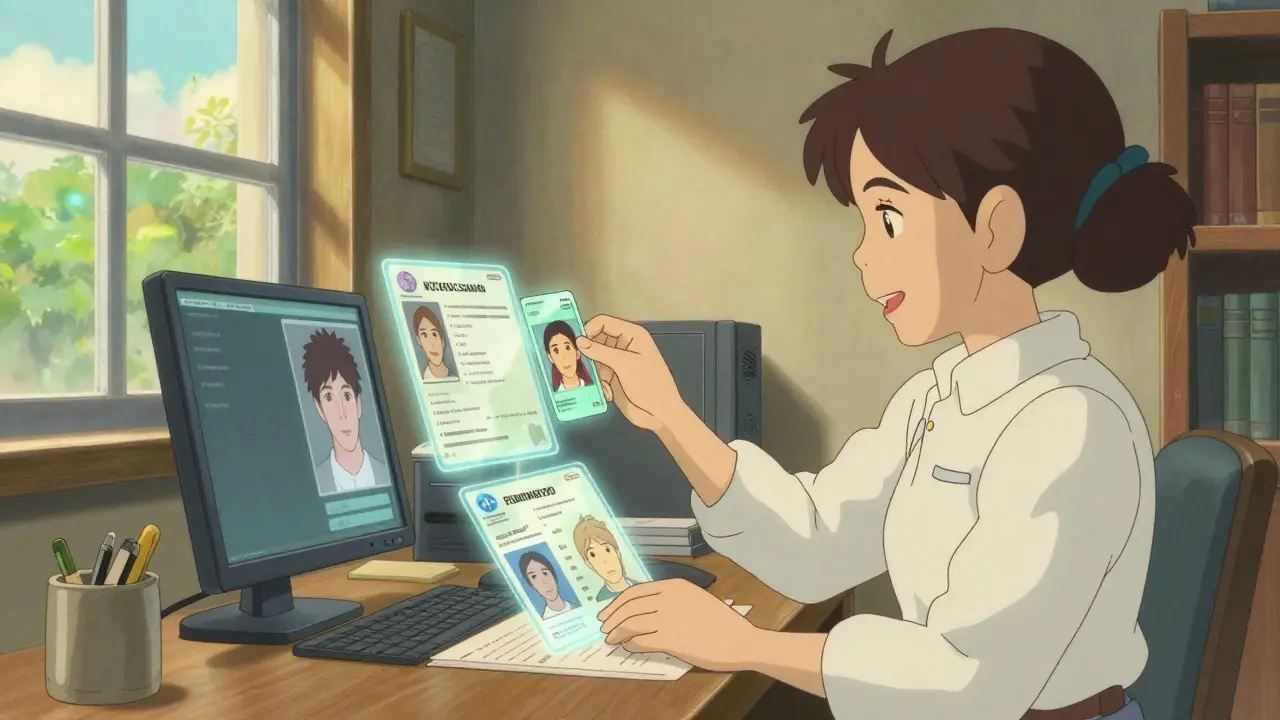

KYC: More Than Just a Photo of Your Passport

You've probably dealt with KYC, known as Know Your Customer, when signing up for an account. While it feels like a chore, it's the foundation of Customer Due Diligence (CDD). It's not just about checking a box; it's about assigning a risk score to every single user.

Modern exchanges use a tiered approach. A user wanting to trade $100 a month might only need a basic email and ID check. But a corporate entity moving millions? They'll undergo "Enhanced Due Diligence," where the exchange digs into the source of wealth and the ultimate beneficial owners. To stop fraud, platforms now use biometric authentication, like liveness detection. This prevents people from simply holding up a photo of someone else's face to the camera to bypass security.

Beyond the ID, exchanges run names against global databases to find Politically Exposed Persons (PEPs) or individuals on sanctions lists. They even use adverse media monitoring-essentially an AI that scans the news to see if a potential client has been linked to financial crimes in the past.

Watching the Flow: Transaction Monitoring Strategies

Once a user is inside, the real work begins. Monitoring crypto is harder than monitoring bank accounts because of the pseudonymous nature of the blockchain. Exchanges use different "strictness levels" depending on their risk appetite and the laws of the country they operate in.

| Approach | How it Works | Strictness | User Friction |

|---|---|---|---|

| Allow Lists | Only pre-verified wallet addresses can send/receive funds. | Extreme | Very High |

| Pattern Analysis | AI flags anomalies in frequency, timing, and amount. | Moderate | Low |

| Deny Lists | Blocks funds coming from known illicit addresses. | Basic | Minimal |

For those using Bitcoin, exchanges look at the UTXO (Unspent Transaction Output) model to trace if coins ever touched a mixer or a darknet market. For stablecoins, the process is often easier because the issuers can sometimes freeze assets directly. The most advanced systems look for "mule" patterns-where a large sum is split into twenty small wallets and then recombined-which is a classic sign of layering in money laundering.

Navigating the Global Regulatory Patchwork

If an exchange operates in both New York and Berlin, they are dealing with two very different sets of rules. In the U.S., the Bank Secrecy Act is the gold standard, focusing heavily on reporting and record-keeping. Meanwhile, the European Union follows directives like the Fifth Anti-Money Laundering Directive (5AMLD), which has its own specific requirements for how digital currency providers must identify their customers.

To handle this, exchanges build dedicated compliance teams. These aren't just lawyers; they are a mix of legal experts and data scientists who can write the rules into the platform's code. These teams must constantly update their policies because a change in a single regulation can make a multi-million dollar feature suddenly illegal.

The High Cost of Getting it Wrong

Some might think, "Why not just skip the AML stuff? It's too expensive." Well, the regulators have made examples out of those who tried. In 2021, one derivatives exchange had to cough up $100 million to settle violations because their AML policies were basically non-existent. In other cases, founders have faced personal fines of $10 million each and the very real threat of prison time for violating the Bank Secrecy Act.

The financial risk isn't just the fines; it's the loss of banking partners. Traditional banks won't touch an exchange that doesn't have a verifiable AML framework. Without a "fiat gateway" to move traditional money in and out, a crypto exchange is essentially a ghost town.

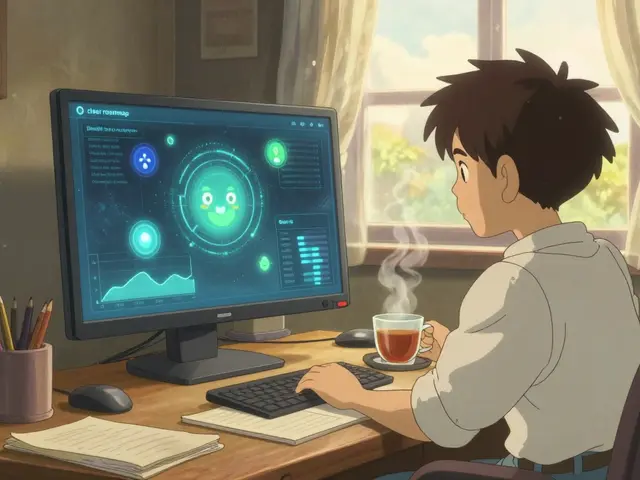

The Future: AI and Scalable Compliance

As the volume of trades grows, humans can't possibly check every transaction. The shift is moving toward "RegTech"-regulatory technology. This includes using flexible APIs and low-code tools that allow compliance officers to change a risk rule in real-time without needing to rebuild the entire app.

We're seeing a move toward dynamic risk scoring. Instead of a static "High" or "Low" risk label, a user's score fluctuates based on their behavior. If you've been a loyal user for three years and suddenly start sending funds to a high-risk offshore entity, your risk score spikes, and the system automatically triggers a request for updated source-of-funds documentation.

Why do crypto exchanges need AML if blockchain is transparent?

While the blockchain is a public ledger, it is pseudonymous. This means you can see that Address A sent money to Address B, but you don't know who owns those addresses. AML processes connect the digital address to a real-world identity, allowing regulators to hold individuals accountable for illegal activities.

What is the difference between KYC and AML?

KYC (Know Your Customer) is a component of AML (Anti-Money Laundering). KYC is the process of verifying a customer's identity. AML is the broader framework of laws and activities-including KYC, transaction monitoring, and reporting-designed to stop the practice of generating income through illegal means.

Can a user avoid AML on a centralized exchange?

On a regulated centralized exchange (CEX), it is nearly impossible to avoid AML. These platforms are legally required to verify identities before allowing deposits or withdrawals. Users seeking more privacy often turn to decentralized exchanges (DEXs), though regulators are increasingly looking for ways to apply similar rules there.

What happens if an exchange detects suspicious activity?

When a system flags a transaction, the compliance team typically conducts a manual review. They may ask the user for more information, such as proof of wealth. If the activity remains suspicious or violates laws, the exchange will freeze the account and file a Suspicious Activity Report (SAR) with the relevant government agency, such as FinCEN in the U.S.

Do all countries follow the same AML rules for crypto?

No, there is a huge variety. While the FATF provides a global baseline, individual countries implement these as different laws. For example, the EU's 5AMLD differs from the U.S. Bank Secrecy Act. This forces global exchanges to build "modular" compliance systems that change based on where the user is located.

Suvoranjan Mukherjee

April 9, 2026 AT 16:20Really great breakdown of the compliance stack! For those getting into this, remember that the interplay between the Travel Rule and KYC is where most of the technical friction happens today. Using Chainalysis or Elliptic for transaction monitoring helps, but you still need a tight API integration to make the onboarding flow seamless for users while keeping the regulators happy. Keep pushing the boundaries of RegTech folks!

Emily 2231

April 10, 2026 AT 01:08THE GOVERNMENT IS JUST USING AML TO MAP EVERY SINGLE TRANSACTION TO A SOCIAL SECURITY NUMBER SO THEY CAN TRACK OUR WEALTH IN REAL TIME. absolute surveillance state. they dont care about money laundering they care about control. wake up people

Arlen Medina

April 10, 2026 AT 21:12Typical govt overreach. We built crypto to get away from this nonsense but now every CEX is just a bank with a different logo. USA should be leading in privacy not helping the SEC choke the life out of innovation

Adriana Gurau

April 11, 2026 AT 11:35Imagine thinking this is a comprehensive guide 🙄. It's cute that you've outlined the basics, but anyone with actual industry experience knows that the gap between FATF guidelines and actual implementation is a chasm of inefficiency. Honestly, the lack of nuance here is just... breathtaking 💅

Bruce Micciulla Agency

April 11, 2026 AT 14:27the whole premise here is flawed because it assumes regulators are actually effective which they arent since most of the volume still flows through offshore entities that barely glance at a passport and the technical side of utxo tracing is basically a game of whack-a-mole where the moles have better software than the cops and we just keep pretending that a risk score means anything when the actual liquidity is moving through unmonitored bridges any way you slice it the system is broken

June Coleman

April 11, 2026 AT 18:55Oh wow, a guide that tells us the government likes to track money. Groundbreaking stuff! 🙄 I'm sure the criminals are shaking in their boots now that we've explained KYC to the internet.

JERRY ORTEGA

April 13, 2026 AT 16:49it is what it is. just use a dex if you want to keep things low key. as long as you arent moving millions the regulators usually dont even blink

david head

April 14, 2026 AT 21:33totally agree with the point about fiat gateways 🚀 without the banks its just a closed loop

shubhu patel

April 16, 2026 AT 16:17I think it is quite fair that the platforms are taking these steps because while privacy is important we cannot ignore that some people use these tools for genuinely terrible things and the tiered approach mentioned here seems like a very reasonable compromise between user experience and legal necessity in the long run

vijendra pal

April 16, 2026 AT 19:12Kyc is so annooying!! 😫 took me 3 days to verify my id on one exchange lol 🤡

Sonya Bowen

April 17, 2026 AT 18:29Compliance is an evolving philosophy. We balance security with liberty.

Earnest Mudzengi

April 17, 2026 AT 23:19CEXs are basically honey pots for the deep state. You give them your ID and then boom, you're on a watchlist because you traded some privacy coins. Total sheep behavior following the BSA rules like it's a holy book. This is how they implement the Great Reset through digital IDs and financial surveillance grids. Absolute madness.

Joshua Aldrich

April 19, 2026 AT 01:06i think the part about the

Joshua Aldrich

April 19, 2026 AT 02:21sorry i meant i think the part about the mulls patterns is super interesting although i think you meant mules. it's crazy how they can track those split transactions now. i read somewhere that some AI can actually predict where the funds are going before they even hit the final wallet. really makes you think about if privacy is even possible anymore in the digital age or if we are just pretending it is while the algorithms watch everything we do in real time with a level of precision that would make the stasi jealous

Nicholas Whooley

April 19, 2026 AT 04:23It is heartening to see the industry moving toward a more standardized and legal framework. This will surely attract more institutional investors who were previously hesitant due to the lack of oversight.

Susan Payne

April 20, 2026 AT 21:23The sheer audacity of suggesting that a

Susan Payne

April 21, 2026 AT 15:26The sheer audacity of suggesting that a few

Susan Payne

April 22, 2026 AT 04:27The sheer audacity of suggesting that a few biometric checks solve the problem of systemic corruption is simply laughable. We are treating the symptoms of a diseased financial system with digital band-aids while the actual architects of fraud continue to operate in the shadows. This entire discourse is a facade of productivity that ignores the moral bankruptcy of the regulatory bodies themselves. I find it utterly exhausting that we must pretend these measures are for our benefit when they are clearly just tools for bureaucratic power plays. The failure to address the core issue of centralized power in these exchanges is a tragedy of modern finance. It is a performance of compliance rather than actual ethics. This is a disaster in the making and the lack of intellectual rigor in the industry is appalling. I cannot believe we are still debating whether

Krystal Moore

April 22, 2026 AT 17:05Literally why is everyone okay with this? Giving a random company in the Seychelles your passport is a nightmare waiting to happen. One leak and your identity is gone. I'm so over this

Susan Wright

April 23, 2026 AT 17:32If you're looking for tools to implement this, check out some of the open-source KYC modules. They save a ton of time during the initial setup phase.

Sharhonda Walker

April 24, 2026 AT 16:06the biometric stuff is laely geting way too invasive. i tried a liveness check and it wouldnt take my photo for ten minutes lol

Robert Coskrey

April 25, 2026 AT 00:09I agree with the assessment of the FATF framework, as it provides a necessary baseline for global stability!!!

Siddharth Bhandari

April 25, 2026 AT 22:05The shift toward RegTech is the only way this scales. Manual reviews are a bottleneck.

Carmelita Gonzales

April 26, 2026 AT 17:13it is a lot to take in but keeping the system safe is worth the extra steps